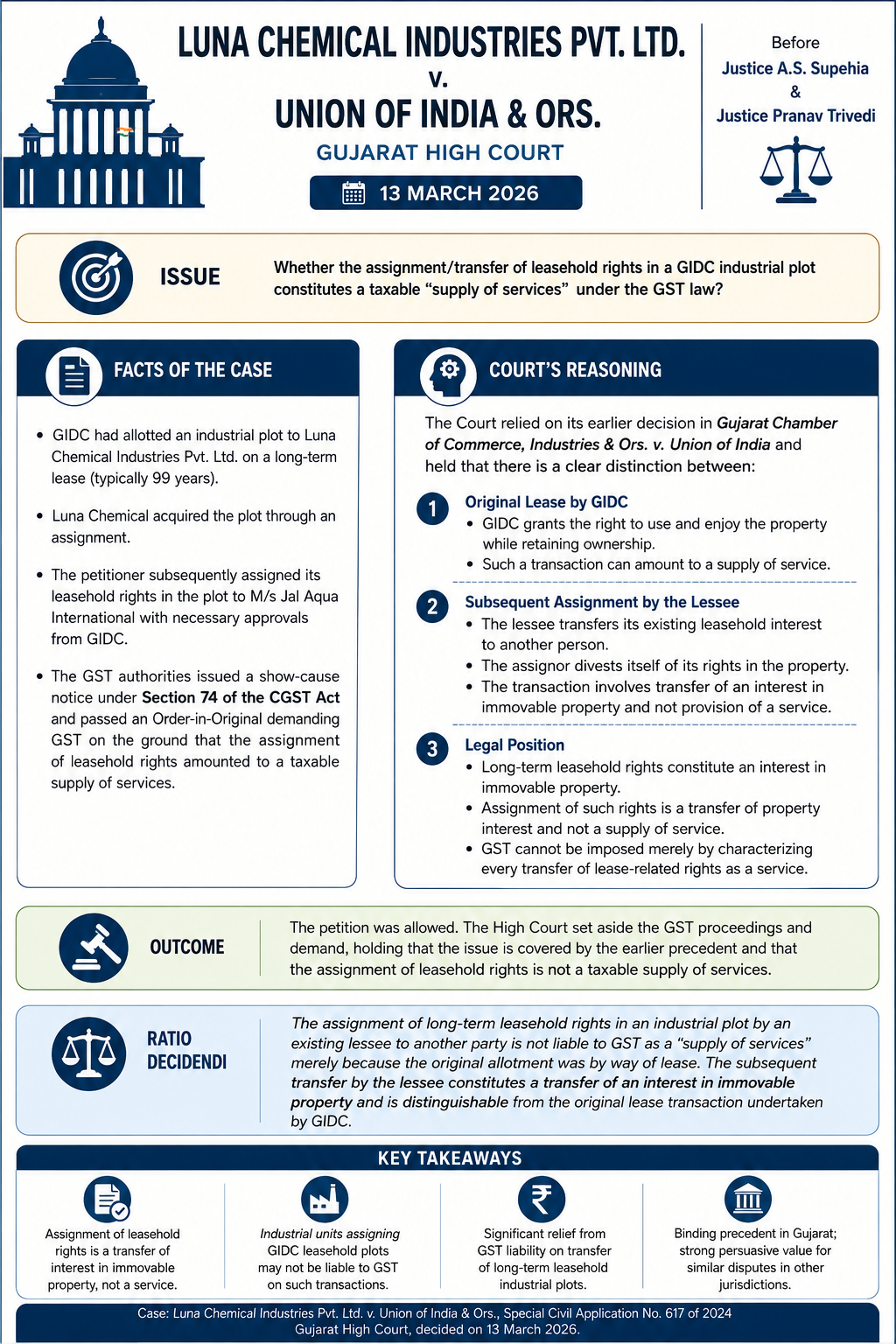

Introduction

The Gujarat High Court’s decision in Luna Chemical Industries Pvt. Ltd. v. Union of India has added another significant chapter to the ongoing debate concerning the GST implications of transfers of leasehold rights in industrial plots. The judgment reaffirms the principle that a transfer of leasehold rights by an existing lessee is fundamentally different from the original grant of lease by a statutory authority and cannot automatically be subjected to GST as a supply of service.

The ruling is particularly relevant for industries operating in Gujarat Industrial Development Corporation (GIDC) estates and for taxpayers involved in the transfer of long-term leasehold interests in industrial land.

Background of the Dispute

Luna Chemical Industries Pvt. Ltd. held leasehold rights in an industrial plot allotted through the GIDC framework. Subsequently, the company assigned its leasehold rights to another entity after obtaining the requisite approvals from GIDC.

The GST authorities initiated proceedings under Section 74 of the Central Goods and Services Tax Act, 2017, alleging that the assignment of leasehold rights constituted a taxable supply of services and consequently raised a demand for GST.

The petitioner challenged the demand before the Gujarat High Court.

CORE LEGAL ISSUE

The principal question before the Court was:

Whether the assignment of leasehold rights in an industrial plot by a lessee to a third party constitutes a taxable supply of services under the GST regime.

The answer depended upon the characterization of the transaction. If the transaction represented a supply of service, GST would be leviable. Conversely, if it constituted a transfer of an interest in immovable property, it would fall outside the scope of taxable supplies.

RATIO DECIDENDI

The Court held that the transfer of leasehold rights by an existing lessee is legally distinct from the original lease granted by GIDC.

The ratio of the decision may be summarized as follows:

The assignment of long-term leasehold rights by a lessee results in the transfer of an existing interest in immovable property and does not amount to a taxable supply of services merely because the original allotment was made through a lease arrangement. Consequently, GST cannot be imposed on such assignment solely by treating it as a continuation of the original leasing transaction.

Distinction between Lease and Assignment

A key aspect of the judgment is the Court’s recognition of the legal distinction between:

- Original Lease by GIDC

- GIDC grants the right to use and enjoy immovable property while retaining ownership.

- Such a transaction may be characterized as a supply of service under GST.

- Subsequent Assignment by the Lessee

- The lessee transfers its existing leasehold interest to another person.

- The assignor divests itself of the rights held in the property.

- The transaction involves transfer of an interest in immovable property rather than provision of a service.

The Court emphasized that these are two separate legal transactions and cannot be treated identically for GST purposes.

Reliance on Earlier Precedent

The judgment follows the Gujarat High Court’s earlier ruling in Gujarat Chamber of Commerce & Industry v. Union of India, where the Court had examined the GST treatment of leasehold interests in industrial plots.

By relying on the principles laid down in the earlier case, the Court maintained consistency in its approach toward characterization of leasehold rights under GST law.

Implications for Industry

The ruling carries significant implications for businesses operating on long-term industrial leases:

- Relief from GST Exposure

Industrial units transferring leasehold rights may rely on the judgment to contest GST demands raised on assignment transactions.

- Recognition of Leasehold Rights as Property Interests

The decision reinforces the jurisprudential view that long-term leasehold rights constitute valuable proprietary interests capable of being transferred independently.

- Reduced Transaction Costs

Assignments of industrial plots often involve substantial consideration. Exclusion of GST from such transactions can significantly reduce the overall cost burden.

- Potential Litigation in Other Jurisdictions

Although the judgment is binding within Gujarat, similar disputes may continue to arise in other States until the issue receives authoritative determination by the Supreme Court or through legislative clarification.

CRITICAL OBSERVATIONS

The judgment aligns with established property law principles recognizing leasehold rights as interests in immovable property. It prevents an overly expansive interpretation of the expression “supply of services” under GST and preserves the distinction between proprietary transfers and service transactions.

At the same time, the decision highlights the continuing tension between traditional property law concepts and the broad charging provisions of GST legislation. Future disputes may focus on the nature and duration of leasehold rights, the terms of assignment, and the extent of control retained by the lessor.

CONCLUSION

The decision in Luna Chemical Industries Pvt. Ltd. v. Union of India represents an important development in GST jurisprudence relating to immovable property transactions. By holding that the assignment of leasehold rights constitutes a transfer of an interest in immovable property rather than a supply of services, the Gujarat High Court has provided much-needed clarity for industrial undertakings and investors dealing with long-term leasehold assets.

The ruling strengthens the principle that the GST consequences of a transaction must be determined based on its true legal character and not merely on the form of the original arrangement from which the rights originate.

SHRUTI DESAI

1 June 2026

Post a comment