Transfers Beyond Statutory Ceiling Limits: Supreme Court Explains the Scope of Section 154 Violations

Supreme Court Clarifies the Nature of Transfers Violating Section 154 of the U.P. Zamindari Abolition and Land Reforms Act: In Arafat Ali (Dead) Through LRs & Ors. v. Deputy Director of Consolidation, Haridwar & Ors. Introduction In a significant judgment delivered on 23 June 2026, the Supreme Court of India in Arafat Ali (Dead) Through Legal Representatives & Others v. Deputy Director of Consolidation, Haridwar & Others settled an important question concerning agricultural land transfers under the Uttar Pradesh Zamindari Abolition and Land Reforms Act, 1950 (“UPZA&LR Act”). The Court examined whether a transfer executed in violation of Section 154 of the Act is void from its inception or merely voidable through appropriate legal proceedings. The ruling provides much-needed clarity for landowners, purchasers, revenue authorities, and practitioners dealing with consolidation and agricultural land disputes in Uttar Pradesh. FACTS OF THE CASE The dispute arose during consolidation proceedings relating to agricultural land transfers allegedly made in contravention of Section 154 of the UPZA&LR Act. The provision restricts acquisition and transfer of agricultural land beyond prescribed statutory limits to prevent excessive concentration of landholdings. The central issue before the Court was whether such transfers automatically become legally non-existent (void ab initio) or continue to have legal effect unless and until challenged before a competent authority. LEGAL ISSUES INVOLVED The Supreme Court was called upon to determine: Whether a transfer of agricultural land made in violation of Section 154 of the UPZA&LR Act is void ab initio or merely voidable under the statutory framework. The answer to this question carries substantial consequences for land titles, mutation entries, consolidation proceedings, and rights of subsequent purchasers. SUPREME COURT’S FINDINGS The Supreme Court held that a transfer made in contravention of Section 154 is not void ab initio. Instead, such a transfer is voidable and remains effective unless it is challenged and set aside through legally prescribed procedures. THE COURT EMPHASIZED THE FOLLOWING PRINCIPLES: Violation of Section 154 Does Not Automatically Nullify the Transfer A transaction executed in breach of the statutory restriction does not cease to exist in the eyes of law merely because the provision has been violated. The transfer continues to operate unless competent proceedings are initiated to invalidate it. Distinction Between Void and Voidable Transactions The judgment reiterates the well-established legal distinction: Void Transaction: A transaction having no legal existence from the very beginning. Voidable Transaction: A transaction that remains valid and enforceable until annulled by a competent authority or court. By classifying transfers violating Section 154 as voidable, the Court protected the principle of legal certainty in property transactions. Applicability of Law Existing on the Date of Transfer The Court observed that the validity of a transfer must ordinarily be assessed with reference to the legal position prevailing on the date of execution of the sale deed or transfer instrument. Appropriate Statutory Remedies Must Be Invoked The Court clarified that challenges to such transfers must be pursued through the mechanisms contemplated under the statute, including proceedings that may be initiated by competent authorities or the Gaon Sabha where applicable. SIGNIFICANCE OF THE JUDGMENT […]

Read more

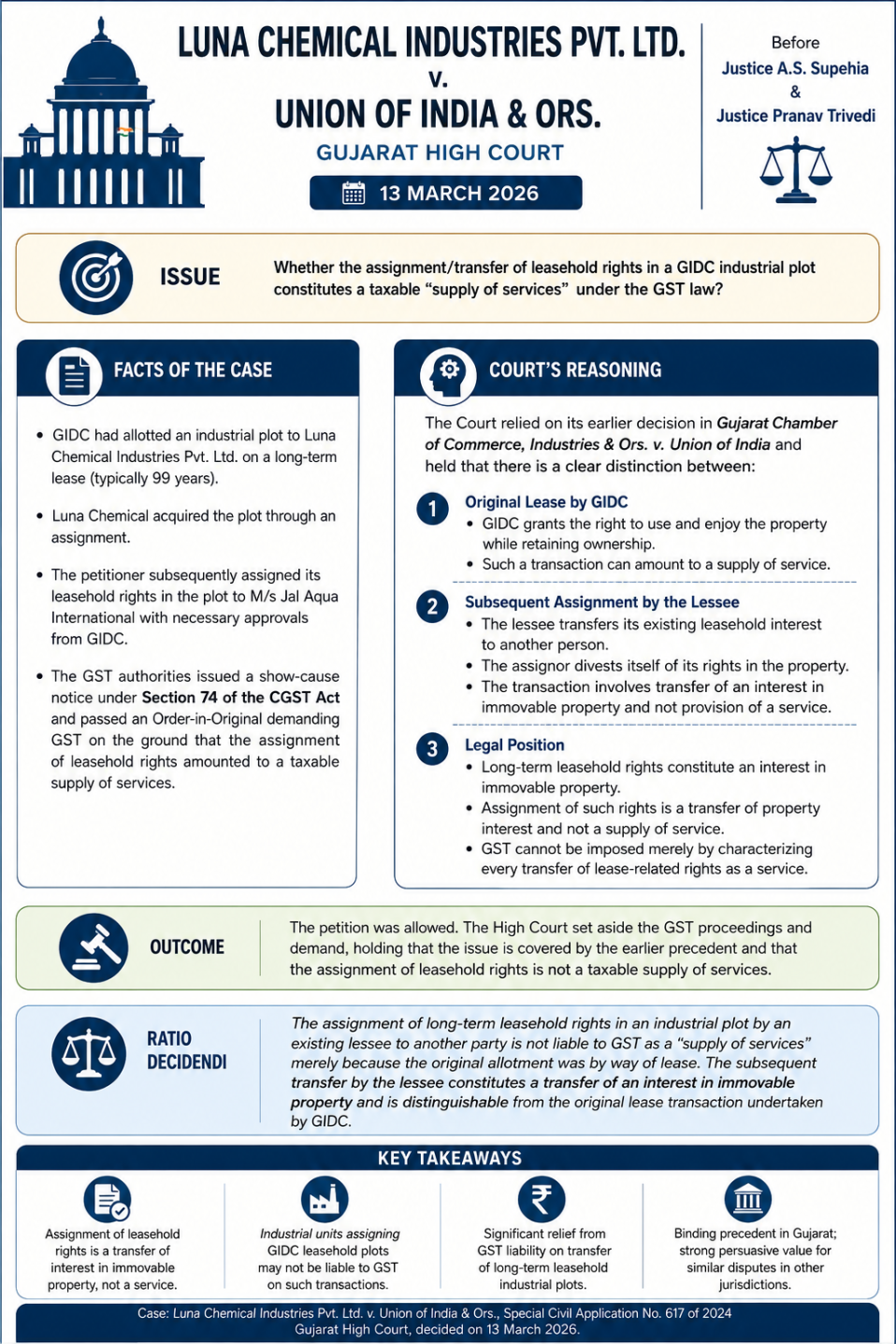

ASSIGNMENT OF LEASEHOLD RIGHTS UNDER GST: ANALYSIS OF LUNA CHEMICAL INDUSTRIES PVT. LTD. V. UNION OF INDIA (GUJARAT HIGH COURT)

Introduction The Gujarat High Court’s decision in Luna Chemical Industries Pvt. Ltd. v. Union of India has added another significant chapter to the ongoing debate concerning the GST implications of transfers of leasehold rights in industrial plots. The judgment reaffirms the principle that a transfer of leasehold rights by an existing lessee is fundamentally different from the original grant of lease by a statutory authority and cannot automatically be subjected to GST as a supply of service. The ruling is particularly relevant for industries operating in Gujarat Industrial Development Corporation (GIDC) estates and for taxpayers involved in the transfer of long-term leasehold interests in industrial land. Background of the Dispute Luna Chemical Industries Pvt. Ltd. held leasehold rights in an industrial plot allotted through the GIDC framework. Subsequently, the company assigned its leasehold rights to another entity after obtaining the requisite approvals from GIDC. The GST authorities initiated proceedings under Section 74 of the Central Goods and Services Tax Act, 2017, alleging that the assignment of leasehold rights constituted a taxable supply of services and consequently raised a demand for GST. The petitioner challenged the demand before the Gujarat High Court. CORE LEGAL ISSUE The principal question before the Court was: Whether the assignment of leasehold rights in an industrial plot by a lessee to a third party constitutes a taxable supply of services under the GST regime. The answer depended upon the characterization of the transaction. If the transaction represented a supply of service, GST would be leviable. Conversely, if it constituted a transfer of an interest in immovable property, it would fall outside the scope of taxable supplies. RATIO DECIDENDI The Court held that the transfer of leasehold rights by an existing lessee is legally distinct from the original lease granted by GIDC. The ratio of the decision may be summarized as follows: The assignment of long-term leasehold rights by a lessee results in the transfer of an existing interest in immovable property and does not amount to a taxable supply of services merely because the original allotment was made through a lease arrangement. Consequently, GST cannot be imposed on such assignment solely by treating it as a continuation of the original leasing transaction. Distinction between Lease and Assignment A key aspect of the judgment is the Court’s recognition of the legal distinction between: Original Lease by GIDC GIDC grants the right to use and enjoy immovable property while retaining ownership. Such a transaction may be characterized as a supply of service under GST. Subsequent Assignment by the Lessee The lessee transfers its existing leasehold interest to another person. The assignor divests itself of the rights held in the property. The transaction involves transfer of an interest in immovable property rather than provision of a service. The Court emphasized that these are two separate legal transactions and cannot be treated identically for GST purposes. Reliance on Earlier Precedent The judgment follows the Gujarat High Court’s earlier ruling in Gujarat Chamber of Commerce & Industry v. Union of India, where the Court had examined the GST treatment of leasehold interests in industrial plots. By relying on the principles laid […]

Read more