Lease or Agreement to Lease? A Case Analysis of Deepak Fertilizers v. Chief Controlling Revenue Authority

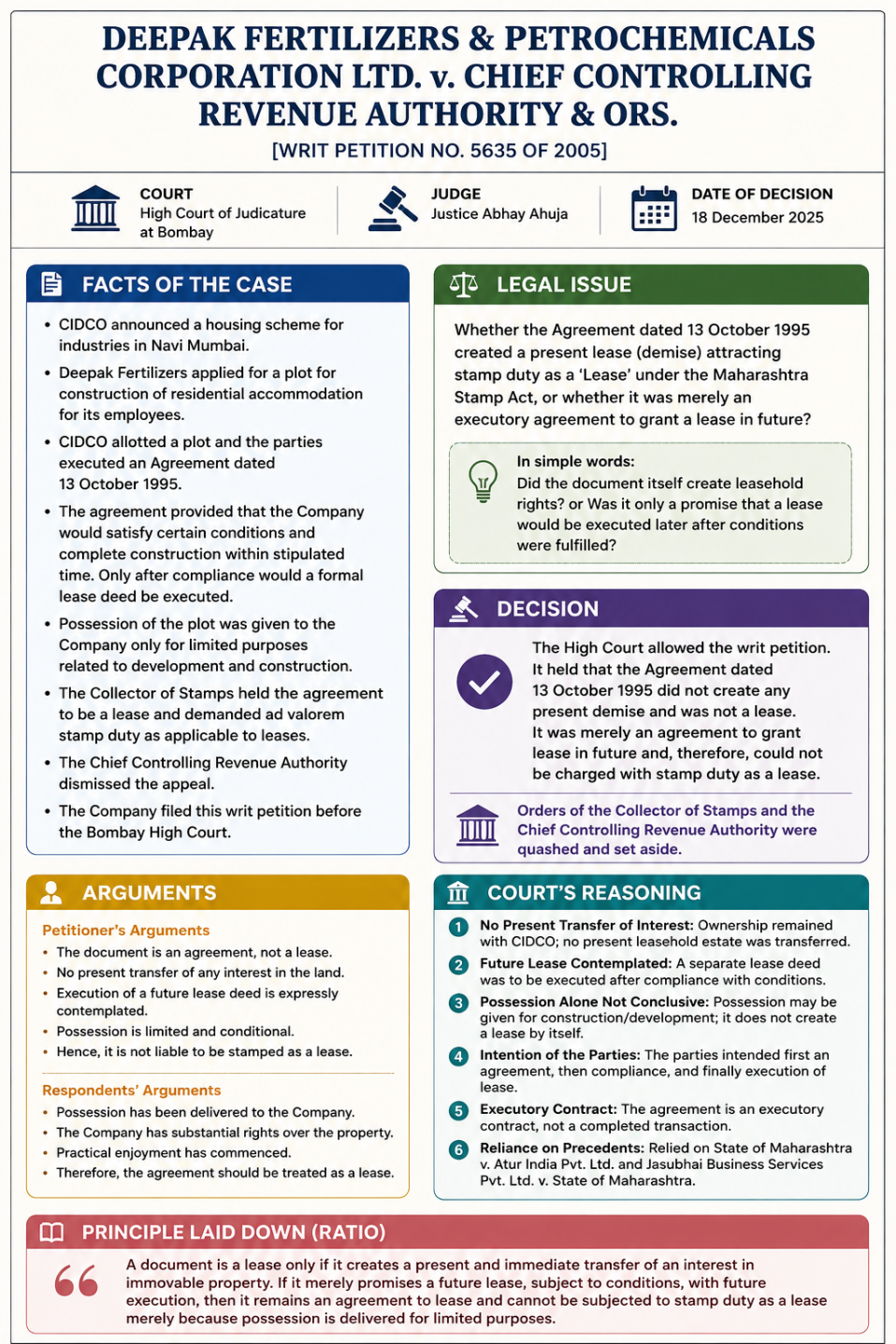

Deepak Fertilizers and Petrochemicals Corporation Ltd. v. Chief Controlling Revenue Authority & Ors., Writ Petition No. 5635 of 2005, decided on 18 December 2025 by Justice Abhay Ahuja. (Verdictum) Background and Facts The dispute arose from an agreement executed on 13 October 1995 between Deepak Fertilizers and CIDCO under a scheme through which CIDCO allotted developed residential plots to industries for construction of staff housing. The material facts were: CIDCO announced a housing scheme for industries in Navi Mumbai. Deepak Fertilizers applied for a plot for construction of residential accommodation for its employees. CIDCO allotted a plot and the parties executed an Agreement dated 13 October 1995. The agreement contemplated that: the company would satisfy several conditions; construction had to be completed within stipulated time; only after compliance would a formal lease deed be executed. Possession given to the company was only for limited purposes connected with development and construction under the agreement. The Collector of Stamps held that the agreement itself amounted to a lease and demanded ad valorem stamp duty as applicable to leases. The Chief Controlling Revenue Authority dismissed the company’s appeal. Deepak Fertilizers challenged those orders before the Bombay High Court. (Verdictum) Procedural History Authority Decision Collector of Stamps Held the agreement was a lease and liable to stamp duty as a lease Chief Controlling Revenue Authority Confirmed Collector’s order Bombay High Court Allowed the writ petition and set aside both orders Legal Issue The central legal issue was: Whether the Agreement dated 13 October 1995 created a present lease (demise) attracting stamp duty as a “Lease” under the Maharashtra Stamp Act, or whether it was merely an executory agreement to grant a lease in future. In simple words: Did the document itself create leasehold rights? or Was it only a promise that a lease would be executed later after conditions were fulfilled? Petitioner’s Arguments Deepak Fertilizers argued that: the document repeatedly described itself as an Agreement; it did not transfer any present interest in land; no leasehold estate came into existence immediately; execution of a future lease deed was expressly contemplated; possession was limited and conditional; therefore the agreement could not be stamped as a lease. The company relied upon earlier Bombay High Court decisions distinguishing between: agreement to lease actual lease Respondents’ Arguments The Revenue and CIDCO contended that: possession had already been handed over; the company had substantial rights over the property; practical enjoyment had commenced; therefore the agreement should be treated as a lease for stamp purposes. Core Legal Question Considered by the Court The Court examined a classical property law distinction: Does the document itself create a present demise? If yes → it is a lease. If no → it is merely an agreement to lease. This distinction has existed in Indian property law for decades. Court’s Reasoning Justice Abhay Ahuja analysed the document clause-by-clause. The Court emphasized that the substance of the document—not merely possession or nomenclature—determines its legal character. (Verdictum) No Present Transfer of Interest The Court observed that: ownership remained with CIDCO; no present leasehold estate was transferred; the agreement only created contractual obligations. This is the most important […]

Read more