H-1B VISA CASE AN ANALYSIS

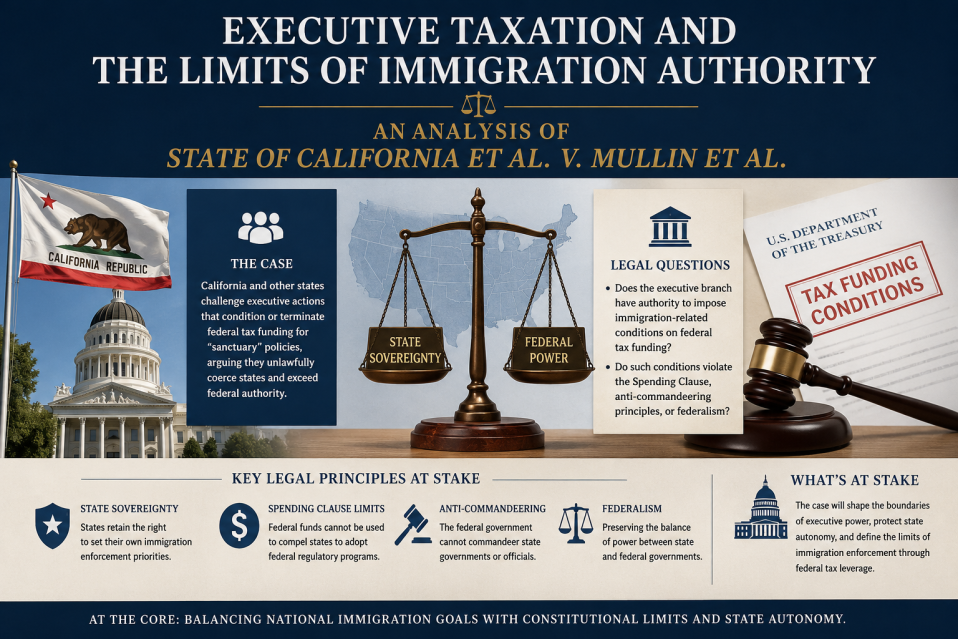

EXECUTIVE TAXATION AND THE LIMITS OF IMMIGRATION AUTHORITY: AN ANALYSIS OF STATE OF CALIFORNIA ET AL. V. MULLIN ET AL. Introduction In State of California et al. v. Mullin et al., U.S. District Judge Leo T. Sorokin invalidated a federal policy requiring employers to pay an additional $100,000 when filing certain H-1B visa petitions. The decision raises important questions regarding the constitutional allocation of taxing authority, the scope of executive power under the Immigration and Nationality Act (INA), and compliance with the Administrative Procedure Act (APA). The Court’s Constitutional Analysis At the center of the dispute was whether the $100,000 payment constituted a permissible regulatory fee or an unauthorized tax. Judge Sorokin concluded that the surcharge functioned as a tax because it was not reasonably related to the government’s costs of processing or administering H-1B petitions. Instead, the payment was designed to influence employer behavior and generate revenue. The court emphasized the Constitution’s allocation of taxing power to Congress. Because Congress had not expressly authorized the executive branch to impose such a charge, the policy violated fundamental separation-of-powers principles. The ruling reinforces the proposition that the executive cannot create new fiscal obligations absent clear legislative authorization. Statutory Authority Under the INA The government argued that Sections 212(f) and 215(a) of the INA provided sufficient authority for the surcharge. These provisions grant the President broad discretion to restrict the entry of non-citizens when deemed detrimental to U.S. interests. The court rejected this interpretation, holding that while the provisions authorize restrictions on entry, they do not authorize the imposition of substantial monetary obligations on domestic employers. The decision reflects judicial reluctance to infer expansive fiscal powers from broadly worded immigration statutes. Administrative Procedure Act Concerns The court further held that the policy violated the APA because it was implemented without notice-and-comment rule-making. The administration relied on guidance documents, memoranda, and related agency materials to establish the surcharge. Judge Sorokin determined that these actions effectively created binding legal obligations and therefore constituted legislative rule-making subject to APA procedural requirements. Additionally, the court found the policy arbitrary and capricious. The government failed to provide a reasoned explanation for selecting the $100,000 amount and did not adequately evaluate the consequences for employers, universities, hospitals, and research institutions. Conclusion The decision serves as a significant reaffirmation of constitutional limits on executive authority. By characterizing the surcharge as a tax rather than a fee, the court underscored Congress’s exclusive role in taxation and signaled that broad immigration powers cannot be used to circumvent legislative control over fiscal policy. Authors view : While the Trump administration did not formally single out Indians in its immigration policies, changes to the H-1B visa program had a disproportionate impact on Indian nationals, who make up the majority of H-1B recipients. Increased fees, tighter scrutiny, and stricter eligibility standards were presented as measures to safeguard American jobs and reduce dependence on foreign labour. Critics contended that these policies created significant challenges for skilled Indian professionals and the technology firms that rely on them. VIEWS OF PRESIDENT OF USA Link to entire case with complaint, motion and Judgment https://www.doj.state.or.us/oregon-department-of-justice/federal-oversight/federal-litigation-tracker/h-1b-visa-petition-fees-california-v-noem-d-mass/?utm_source=chatgpt.com […]

Read more

International Law and the Vulnerabilities of the Global Market

The foundational promise of postwar international economic law was straightforward: establish a rules-based order, and predictable markets would generate shared global prosperity. For decades, multilateral institutions—anchored by the World Trade Organization (WTO), the International Monetary Fund (IMF), and an expansive network of Bilateral Investment Treaties (BITs)—functioned as stabilizing mechanisms for global capital and cross-border trade. Yet the contemporary world economy is increasingly defined not by seamless integration, but by structural fragmentation, geopolitical rivalry, volatile supply chains, and re-surging economic nationalism. As global markets become more vulnerable to political shocks and strategic competition, international legal frameworks are struggling to adapt. Rather than operating as neutral arbiters of trade and investment, these institutions are increasingly transformed into arenas of geopolitical contestation. Geopolitical Power and the Global Economy The global economy is often portrayed as a system governed primarily by trade law, market liberalization, and international cooperation. In practice, however, power politics continues to shape economic outcomes far more profoundly than legal idealism frequently acknowledges. Economic sanctions, military interventions, control over strategic resources, and dominance over global financial infrastructure have become central instruments of international influence. One of the clearest examples is the structural dominance of the United States within the dollar-based global financial system. Since a significant portion of international trade, energy transactions, and sovereign reserves are denominated in U.S. dollars, Washington possesses extraordinary leverage over the global economy. States perceived as challenging American strategic interests can face sanctions, restrictions on banking access, limitations on dollar settlements, and exclusion from critical financial networks. This financial centrality extends American influence far beyond conventional territorial boundaries. India itself experienced the coercive dimension of economic policy following the 1998 Pokhran nuclear tests, when the United States imposed sanctions under its non-proliferation framework. Although India ultimately absorbed these pressures and later developed stronger strategic relations with the United States, the episode illustrated how economic instruments can be mobilized to discipline sovereign states. Similarly, Iran has endured decades of comprehensive sanctions affecting its banking sector, oil exports, trade networks, and broader economic stability. The Iranian case demonstrates how sanctions can evolve from temporary diplomatic measures into long-term geopolitical instruments aimed at strategic containment. Energy politics further intensifies these tensions. Oil-rich regions frequently become focal points of international intervention, proxy conflicts, and political destabilization. Critics argue that major powers often seek to influence resource-rich states either directly through military intervention or indirectly through regime pressure, economic dependency, and geopolitical alignment. At the same time, recent developments indicate that American financial dominance is no longer entirely uncontested. China, Russia, India, and several BRICS members have increasingly explored alternatives to dollar-centric trade mechanisms through local currency settlements, regional payment systems, and efforts toward financial multipolarity. Although the dollar remains dominant, these developments reflect growing dissatisfaction with the concentration of monetary power within a single state. The Iranian experience also reveals the limitations of conventional coercive power. Despite decades of sanctions and diplomatic isolation, Iran has retained significant regional influence and strategic resilience. This underscores the broader reality that modern geopolitical conflicts cannot be resolved solely through economic pressure or military superiority. Consequently, the modern global economy cannot be understood exclusively […]

Read more

From Demonetisation to Digital Currency: How India Led the Global Shift Toward Sovereign Digital Money

From Demonetisation to Digital Currency: How India Led the Global Shift Toward Sovereign Digital Money India is a visionary nation. India had a serious problem of terrorism and funding terrorism through fake currency notes. India, to abate terrorism, opted for demonetisation on 8th November 2016. India introduced digital payment platforms simultaneously. We now have Bharat Pay, G Pay and even every bank has started their UPI. India has shown the world the path towards a digital world. Now, the west side of the globe is following India’s footsteps. USA PASSES LAW OF REGULATORY FRAMEWORK OF DIGITAL CURRENCY: The Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, signed into law in July 2025, establishes the first comprehensive federal regulatory framework for payment stablecoins in the United States. It mandates 100% reserve backing, strict, liquidity requirements, and brings issuers under Bank Secrecy Act (BSA) compliance. Key Aspects of the GENIUS Act (2025-2026): Purpose: To foster innovation in digital assets while protecting consumers and ensuring financial stability. Reserve Requirements: Requires stablecoins to be backed 1:1 by high-quality, liquid assets, such as U.S. dollars or short-term Treasury bills. Issuer Regulation: Only permitted issuers can create payment stablecoins; they must adhere to capital and risk management rules. Consumer Protection: Guarantees redemption rights for stablecoin holders and mandates public disclosures of reserves. Compliance: Subjects issuers to anti-money laundering (AML), countering the financing of terrorism (CFT), and sanction requirements. International Scope: Foreign issuers targeting U.S. users are held to the same standards as domestic issuers. The Treasury Department is actively implementing the law, with public comment periods regarding the regulation of these digital assets extending into late 2025 Overview of U.S. Monetary Evolution The U.S. monetary system has undergone major changes, including: Early issuance of private bank and Treasury currencies. Creation of the Federal Reserve in 1914 as the sole currency issuer. Abandonment of gold and silver convertibility after 1933. These shifts were controversial decisions and actions but are now widely accepted. Emergence of Digital Currencies and CBDC Debate Private digital currencies (e.g., Bitcoin) and foreign CBDCs have prompted U.S. policy debates. A Central Bank Digital Currency (CBDC) is the digital form of a nation’s sovereign currency, issued and regulated by the central bank (e.g., RBI’s “Digital Rupee” or e₹). It acts as legal tender, is interchangeable 1:1 with physical cash, and is designed to make transactions faster, cheaper, and more secure. Key Aspects of CBDCs: Types: Divided into Retail (CBDC-R) for public use and Wholesale (CBDC-W) for interbank settlements. Storage: Held in digital wallets provided by banks, offering 24/7 transactions. Global Status: Over 130 countries, representing 98% of global GDP, are exploring or have launched CBDCs, driven by the need for enhanced digital payment efficiency. Digital Currency Vs. Crypto: Unlike cryptocurrencies, CBDCs are centralised, backed by the state, and not volatile. Goals: Reduce cash-handling costs, improve financial inclusion, and increase cross-border payment efficiency. Key questions include: Whether the Federal Reserve should issue a CBDC. Whether a CBDC would fundamentally change the financial system or simply modernise it. USA Congress has held several hearings and proposed multiple CBDC-related bills in recent sessions. Purpose of the […]

Read more

Digital Euro Initiative: Modernizing Payments and Ensuring Monetary Sovereignty in Europe

Digital Euro Initiative: Modernizing Payments and Ensuring Monetary Sovereignty in Europe European Central Bank (ECB) is driving the digital euro initiative to modernize payments, ensure monetary sovereignty, and complement, not replace, cash. Following completed technical preparations, the project entered a two-year preparation phase in November 2023. A potential rollout is targeted for 2029, with pilot projects expected in 2027 pending legislative approval. Overview • On 28 June, the European Commission proposed legislation to create a legal framework for a digital euro. • The digital euro would be a central bank–issued digital currency designed to complement cash. • It aims to strengthen European retail payments and support the euro’s international role. Objectives • Maintain public access to central bank money in a digital economy. • Respond to declining cash use. • Promote financial inclusion, competition, and innovation. • Enable payments where cash cannot be used, such as online. Relationship with Cash • The digital euro will not replace physical cash. • It is meant to coexist with banknotes and coins. • A parallel proposal protects cash’s legal tender status and accessibility. • Users remain free to choose their payment method. Regulatory Framework • The draft regulation covers: o Legal tender status o Privacy and data protection o Anti-money laundering rules o Distribution and access o Financial stability o International use • The framework is “enabling,” setting core rules without fixing final design details. Digital Euro vs. Bank Deposits • Digital euro: o Issued by the ECB o Liability of the central bank o Similar in nature to cash • Bank account money: o Issued by commercial banks o Private-sector liability • The digital euro may allow offline, proximity payments. Access and User Services • Provided through banks and authorized payment providers. • Alternatives available for people without bank accounts. • Users can switch providers. • Basic services for individuals are free, including: o Account management o Balance checks o Funding and withdrawals o Transfers and payments Privacy Protections • User data handled by service providers, not the ECB. • The ECB will not see users’ identities. • Offline payments offer privacy similar to cash. Holding Limits • Limits may be set to: o Protect monetary and financial stability o Prevent money laundering o Fight terrorism financing Programmability • No automatic restrictions on how money is spent. • Users control how they use their funds. • Conditional payments are possible. Legislative Process and Next Steps • The proposal follows extensive consultations. • It requires approval by the European Parliament and Council. • After adoption, the ECB will decide: o Whether to issue the digital euro o When to launch it o Which design features to adopt Complementary Measures • A separate proposal ensures continued access to cash. • Together, both initiatives aim to guarantee reliable access to public money in all forms. Website: https://www.ecb.europa.eu/euro/digital_euro/html/index.en.html #prof Key aspects of the digital euro : • Strategic Priority: Aimed at strengthening Europe’s financial independence amidst rising private digital currencies and foreign payment solutions. • Key Features: Designed to be a free-of-charge, secure, and instant method for both online and offline payments across the euro area. […]

Read more

Monetary Power in the 21st Century: Theories, and The Rise and Resilience of the Dollar

Monetary Power in the 21st Century: Theories and The Rise and Resilience of the Dollar Printing more dollars hits the US economy hard because it increases the money supply without a corresponding increase in the actual goods and services produced, leading to devaluation and higher prices When the Federal Reserve prints money (or creates it digitally through quantitative easing), it devalues the existing currency, which reduces purchasing power and causes inflation. Here is how printing money hurts the economy: High Inflation: When more money chases the same amount of goods, prices for everyday items rise, as demonstrated in 2021-2022 when high money supply growth led to sharp inflation. Decreased Purchasing Power: As inflation rises, each dollar buys fewer goods and services. This is particularly harmful to consumers, as their wages and savings no longer stretch as far, reducing their standard of living. Erosion of Savings: Inflation act as a “hidden tax” on cash holders. Those with savings, particularly on fixed incomes, see the real value of their money plummet. Loss of Investor Confidence: Excessive, uncontrolled money printing can lead to a loss of faith in the US dollar. If investors believe the currency will continue to lose value, they may shift to more stable assets, reducing the demand for dollars globally. Currency Devaluation Risk: Persistent printing can cause the dollar to weaken against other currencies, making imports more expensive and contributing to trade imbalances. Increased National Debt: When the government prints money to finance spending, it increases the national debt. As the debt grows, it becomes harder for the government to service its obligations without further debasing the currency. Market Bubbles: The influx of money often flows into stocks and real estate rather than into the productive economy, creating asset price bubbles that can lead to financial instability. While printing money can provide a temporary economic boost during a recession, it can cause significant long-term damage if it becomes an addictive tool for handling debt, with historical cases like Germany in the 1920s and Zimbabwe in the 2000s highlighting how it can destroy an economy. THEORY PROPELLED BY VARIOUS ECONOMIST. The concept of printing currency is a highly debated topic among leading economists. On one side, traditional theory stress the importance of maintaining monetary stability, while more modern perspectives support using debt-financed spending to stimulate the economy. At the heart of this debate is the challenge of finding the right balance between leveraging money creation to boost economic activity and managing the potential risks of inflation Here are the primary theories and the authors associated with them: 1. Modern Monetary Theory (MMT) MMT, which gained prominence in the 2010s, argues that governments that issue their own fiat currency (like the US, UK, Japan, and Canada) are not constrained by revenue when it comes to spending. Therefore, they can, and should, print money to fund public services and maintain full employment. Key Authors/Proponents: Warren Mosler (who authored The 7 Deadly Innocent Frauds of Economic Policy and Soft Currency Economics), Stephanie Kelton (The Deficit Myth), L. Randall Wray, and Bill Mitchell. Core Theory: Sovereign governments cannot go broke and do not need […]

Read more

“DE-DOLLARIZATION: DIVERSIFYING FOR A RESILIENT FUTURE”

“DE-DOLLARIZATION: DIVERSIFYING FOR A RESILIENT FUTURE” De-dollarization refers to the process by which countries, institutions, and companies reduce their reliance on the U.S. dollar in international trade, finance, and reserves. In practical terms, it means: Using other currencies (like the euro, yuan, or local currencies) instead of the dollar for trade and payments Holding fewer U.S. dollars in central bank reserves Issuing debt and pricing commodities in non-dollar currencies Settling financial transactions outside the dollar-based system Key idea: Structural vs. Cyclical Demand Structural demand (long-term) This is about the dollar’s role as the world’s main reserve and transaction currency. It includes: Dominance in foreign exchange markets Use in global commodities (oil, gas, metals) Currency used for international loans and bonds Share of global central bank reserves De-dollarization mainly targets this structural role. If it happens meaningfully, the dollar’s global influence weakens over time. Cyclical demand (short-term) This is driven by economic cycles and market trends, such as: Strong U.S. economic growth High U.S. interest rates Strong stock market performance Global investors seeking “safe assets” Recently, strong U.S. performance (“U.S. exceptionalism”) has increased demand for dollars. Investors hold more USD because U.S. assets looked more attractive. A weaker dollar in the future doesn’t automatically mean de-dollarization. It may just reflect changing market conditions. Why countries pursue de-dollarization? As of early 2026, the USA actively imposes financial and trade sanctions via the Office of Foreign Assets Control (OFAC) and Bureau of Industry and Security (BIS). Key targeted countries include Russia, Iran, Cuba, North Korea, Syria, and Venezuela, aiming to restrict trade, influence behavior, and protect national security. Recent actions involve targeting entities linked to Iran’s energy trade, including firms in India, China, and the UAE. Countries may want to reduce dollar dependence to: Avoid U.S. sanctions and financial pressure Reduce exposure to U.S. monetary policy Increase financial sovereignty Strengthen their own currencies Examples include China, Russia, and some BRICS countries promoting trade in local currencies. BRICS SUMMIT 2024 INDIA’S APPROACH ON THE ISSUE The central bank of India, Reserve Bank of India, erstwhile Governor Shaktikanta Das, stated in December 2024 that dedollarization for India was only a part of “derisking” Indian trade and reducing dependence on any one currency since that may become “problematic”. While a BRICS currency had been raised by a member state, nothing specific was decided. He also compared the Euro and stated how nations in Euro countries are located in proximity, while that is not the case with BRICS.This was in response to a question about President-elect Trump warning about tariffs. Former ambassador D. Bala Venkatesh Varma, in an interview with the think tank India Foundation, states that India’s stance in BRICS is “pro-India” and “claiming that BRICS is dominated by China is an exaggeration”. ( wikipedia) US Gold Reserves: Stability, Not Decline US gold reserves have remained unchanged for decades, currently at 8,133.46 tonnes (about $11.041 billion at official valuation). The US remains the world’s largest official holder of gold, accounting for over a quarter of global central bank gold reserves. While the US gold stock is stable, other countries—especially China, Russia, and several emerging markets—have accelerated […]

Read more