Money laundering laws evolved from early record-keeping rules (like the US Bank Secrecy Act, 1970) into a sophisticated global framework, driven by the war on drugs and terrorism, with the FATF (1989) setting global standards (40 Recommendations). Key milestones include the Vienna Convention, US Patriot Act, and EU AML Directives, continually expanding scope to cover new tech like crypto (FATF Rec 15) and closing loopholes in corporate transparency, with laws like India’s PMLA (2002) following global norms.

Early Stages (1970s-1980s)

- Focus: Initial efforts, like the 1970 US Bank Secrecy Act, targeted drug trafficking proceeds, shifting from basic reporting to criminalizing the act itself.

- Motivation: Governments recognized the financial system’s vulnerability and sought tools to seize illicit gains, especially from organized crime.

International Standardization (1989-2000s)

- FATF: The Financial Action Task Force (FATF) was created in 1989, becoming the primary international body issuing guidelines (40 Recommendations) for a unified global approach to combat financial crime.

- United Nations: The Vienna Convention (1988) marked a major early international step, targeting drug-related money laundering.

- Expansion: Efforts broadened beyond drugs to combat terrorist financing, leading to the FATF’s “+9” Special Recommendations and revised 40 Recommendations by 2012.

Modern Era & Technological Challenges (2000s-Present)

EU Directives: The EU’s series of Anti-Money Laundering Directives (AMLDs) progressively strengthened rules on Customer Due Diligence (CDD) and expanded criminal liability.

- USA PATRIOT Act: This significantly enhanced US AML laws post-9/11, increasing scrutiny.

- Digital Assets: In 2019, FATF extended its standards to cover virtual assets (crypto), requiring regulation for Virtual Asset Service Providers (VASPs).

- Beneficial Ownership: Recent FATF updates (2022) focus on combating criminals hiding behind secret corporate structures.

- Global Response: Countries like India (PMLA, 2002) and others enacted laws aligning with these global standards, dealing with issues like fintech and new criminal typologies.

KEY THEMES IN EVOLUTION

- From Banking to All Sectors: Regulations now cover fintech, crypto, and other areas, not just traditional banks.

- Transparency: Moving from a system of trust to one demanding transparency and accountability.

- Adaptability: Laws constantly evolve to counter new criminal methods, from physical cash to digital mixers

- Definition: The process of converting illicit funds (dirty money) into funds with an apparently legal source (clean money).

- Purpose: To use the proceeds from crime without detection by law enforcement, funding further criminal enterprises.

- Stages:

- Placement: Introducing the “dirty” cash into the financial system (e.g., small cash deposits).

- Layering: Obscuring the money’s origin through complex transactions, like electronic transfers or shell companies.

- Integration: Reintroducing the money as legitimate earnings through investments or purchases (e.g., real estate, luxury goods).

Example: The Restaurant Scheme

- A criminal owns a cash-intensive business, like a restaurant or car wash, which generates legitimate revenue.

- They mix illegally obtained cash with the actual daily earnings.

- The business then reports the inflated, combined total as legitimate sales, depositing it into a bank account.

- The money is now “laundered” and appears as ordinary business revenue, making it usable by the criminal.

Other Examples & Methods

- Shell Companies: Creating fake companies to funnel money through.

- Invoice Fraud: Manipulating invoices (over- or under-invoicing) for goods and services to justify moving money.

- Smurfing: Making numerous small cash deposits to avoid triggering reporting requirements.

- Real Estate: Buying and selling properties, often at manipulated values, to move fund.

MONEY LAUNDERING LAWS IN VARIOUS COUNTRIES

INDIA

India’s primary anti-money laundering law is the Prevention of Money Laundering Act (PMLA), 2002, which criminalizes the process of converting illegally obtained money into legitimate funds, allows for asset seizure, and mandates reporting obligations for financial entities like banks, aiming to combat financial crimes and implement UN resolutions. The Directorate of Enforcement (ED), under the Ministry of Finance, investigates and prosecutes offenses, while the Financial Intelligence Unit-India (FIU-IND) coordinates with other agencies and receives transaction reports.

Key Aspects of PMLA:

- Definition of Offence:

Section 3 defines money laundering as any act involving proceeds of crime, including concealment, possession, or projecting them as untainted

- Obligations for Reporting Entities: Banks, financial institutions, and intermediaries must verify client identities, maintain transaction records, and report suspicious or large transactions (e.g., cash over ₹10 Lakhs, cross-border transfers > ₹5 Lakhs) to the FIU-IND.

- Enforcement & Penalties: The ED can attach properties, and offenders face rigorous imprisonment (3-7 years, or up to 10 for certain crimes) and fines. Non-compliant entities can also face fines and license sanctions.

- Adjudication & Appeals: An Adjudicating Authority confirms attachments, and an Appellate Tribunal hears appeals against orders from authorities.

- International Cooperation: India collaborates with international bodies like the FATF to align with global standards.

Regulatory Framework:

- Directorate of Enforcement (ED): Investigates money laundering under PMLA.

- Financial Intelligence Unit-India (FIU-IND): Receives and analyzes reports from reporting entities.

- Sectoral Regulators (e.g., IRDAI for Insurance): Issue specific AML/CFT guidelines for their sectors, ensuring compliance with PMLA.

In essence, PMLA provides the legal backbone, ED enforces it, FIU-IND gathers intelligence, and financial institutions act as gatekeepers, all working to prevent the integration of illicit funds into the legal economy

UK MONEY LAUNDERING LAW is primarily governed by the Proceeds of Crime Act 2002 (POCA), which defines offenses and allows asset recovery, alongside the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLRs), imposing duties on businesses (like customer due diligence, risk assessment, and reporting suspicious activity) to prevent criminals from using services to hide illegal funds. Key obligations include appointing nominated officers, training staff, and maintaining records for several years, with specific rules for different sectors like finance, real estate, and legal services.

Key Legislation:

- Proceeds of Crime Act 2002 (POCA): Broadly defines money laundering as handling “criminal property” (proceeds of crime) and provides the legal framework for prosecuting offenses and seizing criminal assets.

- Money Laundering Regulations 2017 (MLRs) (as amended): Implements international standards (like the EU’s AML Directives) and sets out specific obligations for regulated entities (known as “obliged entities”).

Key Requirements for Businesses:

- Risk Assessment: Conduct firm-wide risk assessments for money laundering and terrorist financing.

- Customer Due Diligence (CDD): Verify customer identities, understand ownership, and monitor transactions.

- Reporting Suspicious Activity: Report suspicions to the National Crime Agency (NCA) via a Suspicious Activity Report (SAR).

- Record Keeping: Maintain records of customer due diligence, transactions, and training for at least five years.

- Designated Personnel: Appoint a Nominated Officer (and potentially a Compliance Officer).

- Training: Provide regular anti-money laundering (AML) training to relevant staff.

Who is Affected?

- Regulated Sector: Financial institutions, legal firms, accountants, estate agents, casinos, etc., are heavily regulated.

- Other Businesses: The MLRs also apply to certain businesses handling high-value cash (e.g., art dealers, car dealers) and other activities at risk of facilitating crime.

Penalties:

- Failure to comply can lead to significant fines, reputational damage, and criminal prosecution for individuals and firms.

In essence, UK law uses POCA to prosecute the crime and the MLRs to place responsibilities on businesses to act as gatekeepers against financial crime.

USA MONEY LAUNDERING LAWS

The main US law against money laundering is the Bank Secrecy Act (BSA), a foundation for financial transparency, heavily updated by the Anti-Money Laundering Act (AMLA) of 2020, which modernized regulations, mandated corporate beneficial ownership reporting (via the Corporate Transparency Act, AML Watcher), and strengthened enforcement for financial institutions. These laws criminalize disguising illegal funds (18 U.S.C. §§ 1956, 1957) and require institutions to implement risk-based AML programs, report suspicious activities (SARs) and large cash transactions (CTRs), and comply with requirements like the beneficial ownership reporting for companies.

Key Legislation & Concepts:

- Bank Secrecy Act (BSA) (1970s):

The bedrock law requiring financial institutions to keep records and report suspicious transactions, preventing misuse of the U.S. financial system for illicit purposes.

- Money Laundering Control Act (1986):

Made money laundering a specific federal crime, adding statutes 18 U.S.C. 1956 and 1957 for prosecuting those who conduct financial transactions with illegal proceeds.

- Anti-Money Laundering Act (AMLA) of 2020:

A major overhaul to modernize U.S. AML/CFT (Countering Financing of Terrorism) efforts, focusing on:

- Corporate Transparency: Requiring disclosure of beneficial ownership (true owners of companies) through the Corporate Transparency Act (CTA) section of the AMLA, FinCEN.gov.

- Enhanced Requirements: Updated rules for banks and businesses to build better risk-based programs and report suspicious activity.

- Whistleblower Protections: Expanded incentives for reporting.

- USA PATRIOT Act (2001):

Expanded BSA requirements, strengthening measures against terrorism financing.

Key Requirements for Businesses:

AML/CFT Programs:

Financial institutions (banks, MSBs, brokers, casinos) must have programs to detect and prevent money laundering.

- Reporting:

File Suspicious Activity Reports (SARs) for transactions over $2,000-$5,000+ and Currency Transaction Reports (CTRs) for cash over $10,000.

- Beneficial Ownership:

Companies must report their beneficial owners to the Financial Crimes Enforcement Network (FinCEN).

ENFORCEMENT:

- The Financial Crimes Enforcement Network (FinCEN) (part of the Treasury) is the primary regulator.

- Violations can lead to severe fines and lengthy prison sentences, often up to 20 years.

LANDMARK JUDGMENTS ON MONEY LAUNDERING IN INDIA

Landmark money laundering cases include international scandals like the HSBC drug cartel laundering case, major corporate frauds such as India’s Satyam & PNB (Nirav Modi) scams, and significant legal battles shaping anti-money laundering (AML) laws, such as India’s Supreme Court upholding the strict bail conditions in the Vijay Madanlal Choudhury v Union of India case, which affirmed the powers of the Enforcement Directorate (ED) under the Prevention of Money Laundering Act (PMLA). These cases highlight the evolution of AML enforcement, the complexities of prosecuting large-scale financial crimes, and judicial interpretations of key legal provisions.

Key International Cases

- HSBC Drug Cartel Case (2012):

HSBC admitted to allowing Mexican drug cartels to launder hundreds of millions through its U.S. subsidiary, exposing major compliance failures.

- 1MDB Scandal:

A massive international embezzlement and money laundering scandal involving Malaysian state fund 1MDB, implicated politicians and financial institutions globally.

- Panama Papers (2016):

A massive leak of confidential financial documents exposing offshore tax havens and potential money laundering by global elites and corporations.

Key Indian Cases and Scandals

The Panama Papers case in India involves investigations into alleged offshore financial dealings of around 500 Indians, including celebrities, politicians, and business figures, exposed in a 2016 leak from Panamanian firm Mossack Fonseca. The Indian government formed a Multi-Agency Group (MAG) involving the CBDT, ED, RBI, and FIU to probe tax evasion and money laundering, leading to cases, searches, tax demands, and prosecutions, with investigations continuing into related leaks like the Paradise and Pandora Papers

Critical note: So far nothing has happened.

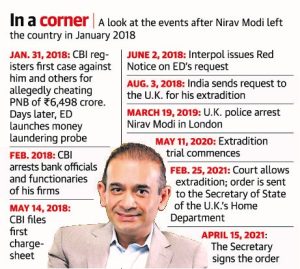

- PNB Scam (Nirav Modi/Mehul Choksi):

Fraudulent transactions worth billions led to the fugitive diamond merchants’ prosecution under PMLA.

- Satyam Scandal (2009):

One of India’s largest accounting frauds, revealing deep-rooted corporate financial manipulation.

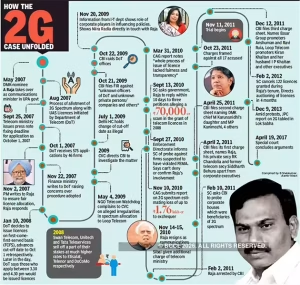

- 2G Spectrum Scam (2010):following picture courtesy Economic Times.

Allegations of illegal allocation of telecom licenses led to significant PMLA investigations. All the Licenses were cancelled but accused are acquitted.

- Vijay Mallya Case:

ED attached properties linked to the defaulting businessman under PMLA for loan defaults.

- Yes Bank-DHFL Case:

Involved criminal conspiracy and offshore fund syphoning related to loan sanctions, leading to charges against Rana Kapoor.

Landmark Legal Judgments (India)

- Vijay Madanlal Choudhury v Union of India (2022):

A three-judge Supreme Court bench upheld crucial provisions of the PMLA, affirming the ED’s extensive powers, including stringent bail conditions, despite earlier challenges.

- Nikkesh Tarachand Sha v Union of India (2017):

The Supreme Court initially found strict bail conditions under PMLA unconstitutional, but this was later negated by parliamentary amendments.

- Arvind Kejriwal v Directorate of Enforcement (Pending):

The Supreme Court is reviewing if the “need and necessity of arrest” is a valid ground to challenge ED arrests under PMLA.

GAMING APP AND MONEY LAUNDERING

Gaming App Money Laundering Case

The gaming app money laundering cases in India highlight the serious implications of unregulated online gaming platforms. The Enforcement Directorate (ED) has been actively cracking down on these scams, arresting individuals involved in money laundering and fraud. Here are some key points from the cases:

- WinZO: The ED arrested co founders Saumya Singh Rathore and Pavaan Nanda for money laundering linked to cheating complaints and a concealed algorithm that used past player performance to match live players with automated gameplay. The company was found to have made ₹177 crore in the past 14 months while causing financial losses to genuine players.

- Probo: The ED attached assets worth ₹117.4 crore linked to Probo Media Technologies, which was alleged to provide a platform for online gambling in the guise of online gaming. The company was found to have defrauded users and made illicit gains through a scheme that falsely presented itself as a skill-based gaming platform.

- Fairplay: The ED claimed that Fairplay ran a sophisticated network of shell and offshore entities involved in money laundering. The app was alleged to have illegally streamed IPL cricket matches and had betting on the 2024 Lok Sabha elections. The proceeds were laundered through bogus imports, fraudulent exports, and overseas investments.

SHRUTI DESAI

20 JANUARY 2026

Post a comment