H-1B VISA CASE AN ANALYSIS

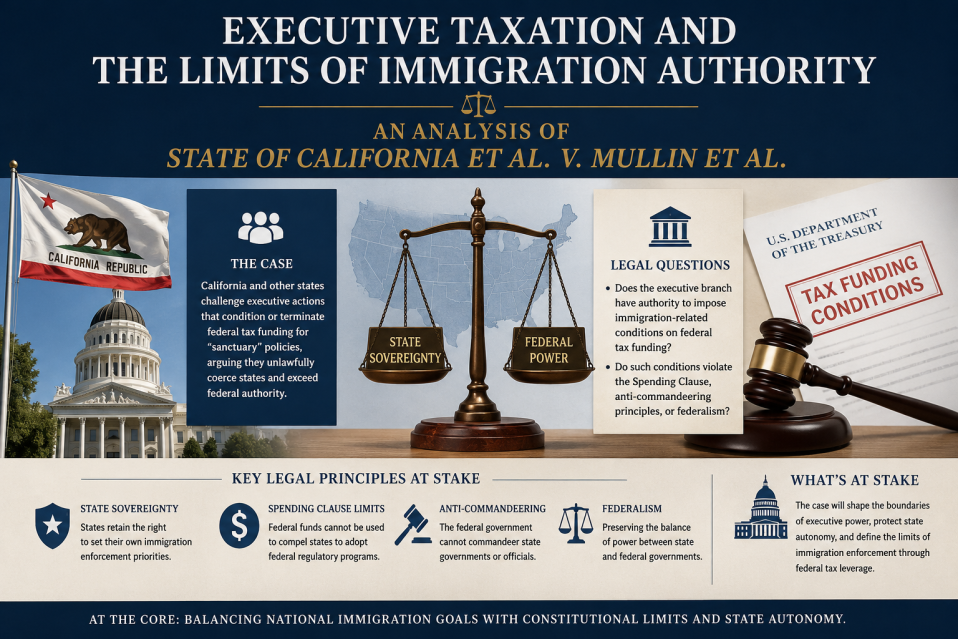

EXECUTIVE TAXATION AND THE LIMITS OF IMMIGRATION AUTHORITY: AN ANALYSIS OF STATE OF CALIFORNIA ET AL. V. MULLIN ET AL. Introduction In State of California et al. v. Mullin et al., U.S. District Judge Leo T. Sorokin invalidated a federal policy requiring employers to pay an additional $100,000 when filing certain H-1B visa petitions. The decision raises important questions regarding the constitutional allocation of taxing authority, the scope of executive power under the Immigration and Nationality Act (INA), and compliance with the Administrative Procedure Act (APA). The Court’s Constitutional Analysis At the center of the dispute was whether the $100,000 payment constituted a permissible regulatory fee or an unauthorized tax. Judge Sorokin concluded that the surcharge functioned as a tax because it was not reasonably related to the government’s costs of processing or administering H-1B petitions. Instead, the payment was designed to influence employer behavior and generate revenue. The court emphasized the Constitution’s allocation of taxing power to Congress. Because Congress had not expressly authorized the executive branch to impose such a charge, the policy violated fundamental separation-of-powers principles. The ruling reinforces the proposition that the executive cannot create new fiscal obligations absent clear legislative authorization. Statutory Authority Under the INA The government argued that Sections 212(f) and 215(a) of the INA provided sufficient authority for the surcharge. These provisions grant the President broad discretion to restrict the entry of non-citizens when deemed detrimental to U.S. interests. The court rejected this interpretation, holding that while the provisions authorize restrictions on entry, they do not authorize the imposition of substantial monetary obligations on domestic employers. The decision reflects judicial reluctance to infer expansive fiscal powers from broadly worded immigration statutes. Administrative Procedure Act Concerns The court further held that the policy violated the APA because it was implemented without notice-and-comment rule-making. The administration relied on guidance documents, memoranda, and related agency materials to establish the surcharge. Judge Sorokin determined that these actions effectively created binding legal obligations and therefore constituted legislative rule-making subject to APA procedural requirements. Additionally, the court found the policy arbitrary and capricious. The government failed to provide a reasoned explanation for selecting the $100,000 amount and did not adequately evaluate the consequences for employers, universities, hospitals, and research institutions. Conclusion The decision serves as a significant reaffirmation of constitutional limits on executive authority. By characterizing the surcharge as a tax rather than a fee, the court underscored Congress’s exclusive role in taxation and signaled that broad immigration powers cannot be used to circumvent legislative control over fiscal policy. Authors view : While the Trump administration did not formally single out Indians in its immigration policies, changes to the H-1B visa program had a disproportionate impact on Indian nationals, who make up the majority of H-1B recipients. Increased fees, tighter scrutiny, and stricter eligibility standards were presented as measures to safeguard American jobs and reduce dependence on foreign labour. Critics contended that these policies created significant challenges for skilled Indian professionals and the technology firms that rely on them. VIEWS OF PRESIDENT OF USA Link to entire case with complaint, motion and Judgment https://www.doj.state.or.us/oregon-department-of-justice/federal-oversight/federal-litigation-tracker/h-1b-visa-petition-fees-california-v-noem-d-mass/?utm_source=chatgpt.com […]

Read more