Insolvency and bankruptcy Code,2016 was enforced with big bang and with hope. Let us first understand the relevant provisions of the law which is subject of discussion here.

The Preamble of the Act indicates purpose of enactment. It says, “ An Act to consolidate and amend the laws relating to reorganisation and insolvency resolution of corporate persons, partnership firms and individuals in a time bound manner for maximisation of value of assets of such persons, to promote entrepreneurship, availability of credit and balance the interests of all the stakeholders including alteration in the order of priority of payment of Government dues and to establish an Insolvency and Bankruptcy Board of India, and for matters connected therewith or incidental thereto.”

The provisions of this Code shall apply to— (a) any company incorporated under the Companies Act, 2013 or under any previous company law; (b) any other company governed by any special Act for the time being in force, except in so far as the said provisions are inconsistent with the provisions of such special Act; (c) any Limited Liability Partnership incorporated under the Limited Liability Partnership Act, 2008; (d) such other body incorporated under any law for the time being in force, as the Central Government may, by notification, specify in this behalf; and (e) partnership firms and individuals, in relation to their insolvency, liquidation, voluntary liquidation or bankruptcy, as the case may be.

“creditor” means any person to whom a debt is owed and includes a financial creditor, an operational creditor, a secured creditor, an unsecured creditor and a decree holder;

“debt” means a liability or obligation in respect of a claim which is due from any person and includes a financial debt and operational debt;

“default” means non-payment of debt when whole or any part or instalment of the amount of debt has become due and payable and is not repaid by the debtor or the corporate debtor, as the case may be.

“operational creditor” means a person to whom an operational debt is owed and includes any person to whom such debt has been legally assigned or transferred;

“operational debt” means a claim in respect of the provision of goods or services including employment or a debt in respect of the repayment of dues arising under any law for the time being in force and payable to the Central Government, any State Government or any local authority;

- Submission of resolution plan. – (1) A resolution applicant may submit a resolution plan [along with an affidavit stating that he is eligible under section 29A] to the resolution professional prepared on the basis of the information memorandum.(2) The resolution professional shall examine each resolution plan received by him to confirm that each resolution plan- (a) provides for the payment of insolvency resolution process costs in a manner specified by the Board in priority to the [payment] of other debts of the corporate debtor; [(b) provides for the payment of debts of operational creditors in such manner as may be specified by the Board which shall not be less than – (i) the amount to be paid to such creditors in the event of a liquidation of the corporate debtor under section 53; or (ii) the amount that would have been paid to such creditors, if the amount to be distributed under the resolution plan had been distributed in accordance with the order of priority in sub-section (7) of section 53,whichever is higher, and provides for the payment of debts of financial creditors, who do not vote in favour of the resolution plan, in such manner as may be specified by the Board, which shall not be less than the amount to be paid to such creditors in accordance with sub-section (7) of section 53 in the event of a liquidation of the corporate debtor.

Explanation 1. – For the removal of doubts, it is hereby clarified that a distribution in accordance with the provisions of this clause shall be fair and equitable to such creditors.

Explanation 2. – For the purposes of this clause, it is hereby declared that on and from the date of commencement of the Insolvency and Bankruptcy Code (Amendment) Act, 2019, the provisions of this clause shall also apply to the corporate insolvency resolution process of a corporate debtor –

(i) where a resolution plan has not been approved or rejected by the Adjudicating Authority;

(ii) where an appeal has been preferred under section 61 or section 62 or such an appeal is not time barred under any provision of law for the time being in force; or

(iii) where a legal proceeding has been initiated in any court against the decision of the Adjudicating Authority in respect of a resolution plan;]

(c) provides for the management of the affairs of the Corporate debtor after approval of the resolution plan;

(d) the implementation and supervision of the resolution plan;

(e) does not contravene any of the provisions of the law for the time being in force;

(f) conforms to such other requirements as may be specified by the Board.

[Explanation. – For the purposes of clause (e), if any approval of shareholders is required under the Companies Act, 2013 or any other law for the time being in force for the implementation of actions under the resolution plan, such approval shall be deemed to have been given and it shall not be a contravention of that Act or law.]

(3) The resolution professional shall present to the committee of creditors for its approval such resolution plans which confirm the conditions referred to in sub-section (2).

[(4) The committee of creditors may approve a resolution plan by a vote of not less than [sixty-six] per cent. of voting share of the financial creditors, after considering its feasibility and viability [the manner of distribution proposed, which may take into account the order of priority amongst creditors as laid down in sub-section (7) of section 53, including the priority and value of the security interest of a secured creditor] and such other requirements as may be specified by the Board:

Provided that the committee of creditors shall not approve a resolution plan submitted before the commencement of the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2017, where the resolution applicant is ineligible under section 29A and may requires the resolution professional to invite a fresh resolution plan where no other resolution plan is available with it.

Provided further that where the resolution applicant referred to in the first proviso is ineligible under clause (c) of section 29A, the resolution applicant shall be allowed by the committee of creditors such period not exceeding thirty days to make payment of overdue amount in accordance with the proviso to clause (c) of section 29A.

Provided also that nothing in the second proviso shall be construed as extension of period for the purposes of the proviso to sub-section (3) of section 12 and the corporate insolvency resolution process shall be completed within the period specified in that sub-section].

[Provided also that the eligibility criteria in section 29A as amended by the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2018 (ord. 6 of 2018) shall apply to the resolution applicant who has not submitted resolution plan as on the date of commencement of the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2018 (ord. 6 of 2018).]

(5) The resolution applicant may attend the meeting of the committee of creditors in which the resolution plan of the applicant is considered:

Provided that the resolution applicant shall not have a right to vote at the meeting of the committee of creditors unless such resolution applicant is also a financial creditor.

(6) The resolution professional shall submit the resolution plan as approved by the committee of creditors to the Adjudicating Authority.

- Approval of resolution plan. – (1) If the Adjudicating Authority is satisfied that the resolution plan as approved by the committee of creditors under sub-section (4) of section 30 meets the requirements as referred to in sub-section (2) of section 30, it shall by order approve the resolution plan which shall be binding on the corporate debtor and its employees, members, creditors, [including the Central Government, any State Government or any local authority to whom a debt in respect of the payment of dues arising under any law for the time being in force, such as authorities to whom statutory dues are owed,] guarantors and other stakeholders involved in the resolution plan.

[Provided that the Adjudicating Authority shall, before passing an order for approval of resolution plan under this sub-section, satisfy that the resolution plan has provisions for its effective implementation.]

(2) Where the Adjudicating Authority is satisfied that the resolution plan does not confirm to the requirements referred to in sub-section (1), it may, by an order, reject the resolution plan.

(3) After the order of approval under sub-section (1),-

(a) the moratorium order passed by the Adjudicating Authority under section 14 shall cease to have effect; and

(b) the resolution professional shall forward all records relating to the conduct of the corporate insolvency resolution process and the resolution plan to the Board to be recorded on its database.

[(4) The resolution applicant shall, pursuant to the resolution plan approved under sub-section (1), obtain the necessary approval required under any law for the time being in force within a period of one year from the date of approval of the resolution plan by the Adjudicating Authority under sub-section (1) or within such period as provided for in such law, whichever is later:

Provided that where the resolution plan contains a provision for combination, as referred to in section 5 of the Competition Act, 2002, the resolution applicant shall obtain the approval of the Competition Commission of India under that Act prior to the approval of such resolution plan by the committee of creditors.]

Section 76. Where— (a) an operational creditor has wilfully or knowingly concealed in an application under section 9 the fact that the corporate debtor had notified him of a dispute in respect of the unpaid operational debt or the full and final repayment of the unpaid operational debt; or (b) any person who knowingly and wilfully authorised or permitted such concealment under clause (a), such operational creditor or person, as the case may be, shall be punishable with imprisonment for a term which shall not be less than one year but may extend to five years or with fine which shall not be less than one lakh rupees but may extend to one crore rupees, or with both.

Comments :

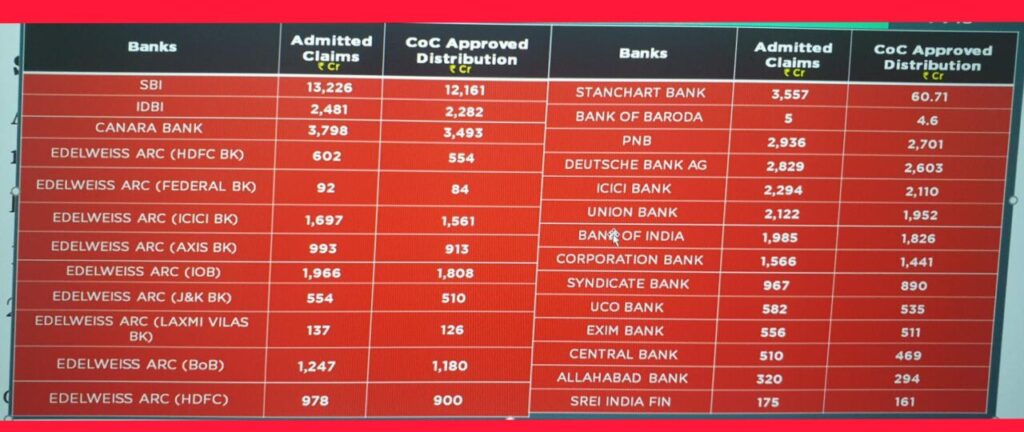

In 2019 Section 30-31 was amended here I have provided amended Section. While reading the provisions of Section the plan of is sanctioned and approved by Committee of Creditors. This Committee has majority members of banking consortium who has give huge loans. Adjudicating authority has not much to say once plan is approved. The very purpose of the law is mired which is seen in below table:

Here is list available on various media website :

We can see haircut of 60 to 80% is availed by the Committee of Operational Creditors. After paying the approved amount the defaulters are absolved of all criminal and tax liabilities.

In the Rajya Sabha debates, on 29.7.2019, when the Bill for amending I&B Code came up for discussion, there were certain issues raised by certain Members. While replying to the issues raised by certain Members, the Hon’ble Finance Minister stated thus:

“IBC has actually an overriding effect. For instance, you asked whether IBC will override SEBI. Section 238 provides that IBC will prevail in case of inconsistency between two laws. Actually, Indian courts will have to decide, in specific cases, depending upon the material before them, but largely, yes, it is IBC. […] There is also this question about indemnity for successful resolution applicant. The amendment now is clearly making it binding on the Government. It is one of the ways in which we are providing that. The Government will not raise any further claim. The Government will not make any further claim after resolution plan is approved. So, that is going to be a major, major sense of assurance for the people who are using the resolution plan. Criminal matters alone would be proceeded against individuals and not company. There will be no criminal proceedings against successful resolution applicant. There will be no criminal proceedings against successful resolution applicant for fraud by previous promoters. So, I hope that is absolutely clear. I would want all the hon. Members to recognize this message and communicate further that this Code, therefore, gives that comfort to all new bidders. So now, they need not be scared that the taxman will come after them for the faults of the earlier promoters. No. Once the resolution plan is accepted, the earlier promoters will be dealt with as individuals for their criminality but not the new bidder who is trying to restore the company. (excerpts from speech)

Dictum: Hence once plan is approved the defaulter comes out clean.

Due Diligence by lenders – banks :

It needs hardly any emphasis that in the ordinary course of their business, when the bankers or financial institutions examine any proposal for loan or advance or akin facility, they are supposed to, and they indeed, take up the exercise commonly termed as ‘due diligence’ so as to study the viability of the proposed enterprise as also to ensure, inter alia, that the security against such loan/advance/facility is genuine and adequate; and would be available for enforcement at any point of time. Given the nature of transaction, the lenders must prefer a clean security to justify the transaction as being in the ordinary course of their business. In the same exercise, in the ordinary course of their business, if they are at all entering into a transaction whereby a third-party security, including that of a subsidiary company, is to be taken as collateral, they are obliged to undertake further due diligence. ( Supreme Court in Anuj Jain Supra)

The term ‘due diligence’ is explained in P. Ramanatha Aiyar’s Advanced Law Lexicon (5th Ed.-Vol 2, p.1654) in the following:

“The detailed review of the borrower/issuer’s overall position, which is supposed to be undertaken by the lead manager of a new financing in conjunction with the preparation of legal documentation.

Analysis of the financial status and prospects of company before it receives a major investment of capital. It is usually carried out by an independent accountant.” that such third-party security is a prudent and viable one and is not likely to be hit by any law. In that sequence, they remain under obligation to assure themselves that such third party whose security is being taken, is not already indebted or in red and is not likely to fail in dealing with its own indebtedness. In the context of IBC, such requirement is moreover imperative on a bare look at the provisions contained in Part II thereof.

Our banks lend crores of rupees and the promoters make default despite of due diligence which is seen from the table given above.

Let us see what is opinion of Courts.

Judgment :

Ghanshyam Mishra and Sons Pvt. Ltd. v. Edelweiss Asset Reconstruction Company Limited, decided on 13.04.2021 by Supreme Court on Section 30 and 31 observed as under:

- Perusal of the SOR would reveal, that one of the prime objects of I&B Code was to provide for implementation of insolvency resolution process in a time bound manner for maximisation of value of assets in order to balance the interests of all stakeholders. However, it was noticed, that in some cases there was extensive litigation causing undue delays resultantly hampering the value maximisation. It was also found necessary to ensure, that all creditors are treated fairly. It was therefore in view of the various difficulties faced and in order to fill the critical gaps in the corporate insolvency framework, it was necessary to amend certain provisions of the I&B Code. Clause (f) of para 3 of the SOR of the Insolvency and Bankruptcy Code (Amendment) Bill, 2019 would amply make it clear, that the legislative intent in amending subsection (1) of Section 31 of I&B Code was to clarify, that the resolution plan approved by the Adjudicating Authority shall also be binding on the Central Government, any State Government or any local authority to whom a debt is owed in respect of payment of dues arising under any law for the time being in force, such as authorities to whom statutory dues are owed, including tax authorities.

MORTGAGE DEBT AND UNDERVALUED TRANSACTION SUPREME COURT

Anuj Jain vs. Axis Bank Limited on 26 February, 2020

For holding a transaction undervalued, the Resolution Professional/Liquidator is required to examine the transactions which were made during the relevant period as prescribed under Section 46, if any of it is undervalued. As per sub-section (2) of Section 45, the transaction shall be considered undervalued where the Corporate Debtor makes a gift to a person or enters into a transaction with a person which involves the transfer of one or more assets by the Corporate Debtor for a consideration the value of which is significantly less than the value of the consideration provided by the Corporate Debtor and such transaction has not taken place in the ordinary course of business of the Corporate Debtor.

As Section 44 is not attracted, it is not necessary to notice Section 46 which is not attracted and, therefore, the Adjudicating Authority has no power to pass any order under Section 48 of the I&B Code. With respect to Section 66 of the Code dealing with fraudulent trading or wrongful trading, the Appellate Tribunal observed that the corporate debtor, being one of the group company, like a guarantor, had executed mortgage deeds in favour of the lender banks and financial institutions; and the transactions were in the ordinary course of business of the corporate debtor.

Fair and equitable dealing of operational creditors rights under the said Regulation involves the resolution plan stating as to how it has dealt with the interests of operational creditors, which is not the same thing as saying that they must be paid the same amount of their debt proportionately. Also, the fact that the operational creditors are given priority in payment over all financial creditors does not lead to the conclusion that such payment must necessarily be the same recovery percentage as financial creditors. So long as the provisions of the Code and the Regulations have been met, it is the commercial wisdom of the requisite majority of the Committee of Creditors which is to negotiate and accept a resolution plan, which may involve differential payment to different classes of creditors, together with negotiating with a prospective resolution applicant for better or different terms which may also involve differences in distribution of amounts between different classes of creditors.

SCOPE AND JURISDICTIONS OF ADJUDICATING AUTHORITY

CIVIL APPEAL NO. 3395 OF 2020 JAYPEE KENSINGTON BOULEVARD APARTMENTS WELFARE ASSOCIATION & ORS. VERSUS NBCC (INDIA) LTD. & ORS supreme court held that; The Adjudicating Authority has limited jurisdiction in the matter of approval of a resolution plan, which is well-defined and circumscribed by Sections 30(2) and 31 of the Code. In the adjudicatory process concerning a resolution plan under IBC, there is no scope for interference with the commercial aspects of the decision of the CoC; and there is no scope for substituting any commercial term of the resolution plan approved by Committee of Creditors. If, within its limited jurisdiction, the Adjudicating Authority finds any shortcoming in the resolution plan vis-à-vis the specified parameters, it would only send the resolution plan back to the Committee of Creditors, for re-submission after satisfying the parameters delineated by the Code and exposited by this Court.

Videocon IA 196 of 2021 NCLT Relying on Judgement in Ghanashyam Mishra and Sons Private Limited (Supra) NCLT approved proposed Resolution Plan which meets the requirements of Section 30(2) of the Code and Regulations 37, 38, 38(1A) and 39 (4) of the Regulations. The Resolution Plan is not found in contravention of any of the provisions of Section 29A of the Code and is in accordance with Law.

The consortium of creditors settled with 96% of haircut. “Out of total claim amount of Rs 71,433.75 crore, claims admitted are for Rs 64,838.63 crore and the plan is approved for an amount of only Rs 2,962.02 crore, which is only 4.15 per cent of the total outstanding claim amount and the total hair cut to all the creditors is 95.85 per cent,” the NCLT observed vide order dated 8th June,2021

Essar steel case:

Source Moneycontrol:

Suggestions by Author :

As seen in table above against Rs.2654 million, Rs.1146 million is recovered. There is also representation that it resulted into job loss.

IBC needs immediate amendment :

- Operational Creditor Committee shall not decide haircut

- There should be law to sanction #Haircut It cannot be 90 to 95%

- There should be reserve bid for minimum price and it should be placed on public portal of #NCLT

- Government followed the process of inviting global tenders in Coal Mine auction and 2G License same method must be followed

- Institute inquiry why 90 % reduction in value was permitted by misusing law ?

Shruti Desai

7th July,2021

Post a comment